Despite growing market hopes for multiple rate cuts, the US Federal Reserve (Fed) has made one thing clear: interest rates are likely to stay elevated well into 2025.

The current Federal Funds rate stands at 4.25% to 4.50%, slightly lower than its peak but still well above pre-pandemic levels [1].

While inflation has moderated and economic growth has cooled, the Fed remains cautious, choosing to hold rates steady rather than risk undoing progress with premature easing.

The message is consistent: progress on inflation has been encouraging, but not yet sufficient to warrant a more aggressive pivot. The Fed’s priority now is to avoid a repeat of past mistakes: cutting too early, reigniting inflation, and losing hard-won credibility.

This cautious stance follows one of the most aggressive tightening campaigns in decades, launched in response to a post-pandemic surge in inflation. After bringing rates down slightly in late 2024, the Fed has since opted to pause, signaling its intention to keep policy restrictive until inflation expectations are firmly under control.

For investors, this “higher for longer” environment means the era of cheap money is not returning as quickly as hoped. Rate-sensitive sectors like property, small caps, and speculative tech remain under pressure, while defensives and high-quality dividend-paying stocks are often seen as more resilient in such environments.

Yet the economy has remained surprisingly resilient, supported by strong household balance sheets, steady job growth, and corporate earnings that have weathered the tightening cycle better than feared. In this new environment, understanding the Fed’s reluctance to ease too soon is key to navigating markets in the second half of 2025 and beyond.

In this article, we dive into the rationale behind the Fed’s decision, how previous high-rate cycles played out, sector-specific risks and opportunities, and what this could mean globally. Focusing solely on the timing of rate cuts may overlook broader market developments and underlying structural trends.

Key Points

- The Fed is keeping rates high in 2025 to avoid premature easing and ensure inflation stays under control.

- Markets face uneven impacts, with sectors like tech and real estate under pressure, while defensives gain appeal.

- Some analysts suggest that looking beyond rate cuts and examining broader macro trends, including sector shifts and global developments, may offer a fuller picture of market conditions.

Why the Fed is holding rates steady [2,3.4]

Behind the Fed’s reluctance to ease monetary policy lies a complex mix of sticky inflation, a still-strong labour market, and rising geopolitical uncertainty. Although headline inflation has moderated, core price pressures remain persistent, particularly in services and wage-sensitive categories.

At the same time, employment remains solid, with the unemployment rate near 4.2% and April job gains totaling 177,000, leaving the Fed in no rush to stimulate growth further.

Fed Chair Jerome Powell underscored the Fed’s data-driven patience, stating, “We think we’re in the right place to wait and see how things evolve. We don’t feel like we need to be in a hurry. We feel like it’s appropriate to be patient”.

He added that preemptive moves could risk losing control over inflation expectations, which the Fed has spent years working to anchor as he stated that “It’s not a situation where we can be preemptive, because we actually don’t know what the right response to the data will be until we see more data.”

One of the most significant developments clouding the Fed’s outlook is the re-emergence of tariff-driven inflation risks. President Trump’s new wave of import duties, still under negotiation but already affecting sentiment, has injected fresh volatility into markets and the macroeconomic backdrop.

Powell cautioned that if these tariffs are sustained, “they’re likely to generate a rise in inflation, a slowdown in economic growth and an increase in unemployment.” While the inflationary impact could be short-lived, Powell warned it’s “also possible that the inflationary effects could instead be more persistent.”

The Federal Open Market Committee (FOMC) acknowledged these risks in its May statement, saying “the risks of higher unemployment and higher inflation have risen.” Businesses are already reacting, with many frontloading imports and delaying investment decisions, and consumers showing signs of pulling forward spending.

The Fed, wary of this evolving situation, is opting to hold rates until the economic picture becomes clearer. Powell emphasised that the central bank is “in the right place to wait and see,” stressing that policymakers will stay data-dependent and avoid preemptive moves until the outlook becomes clearer.

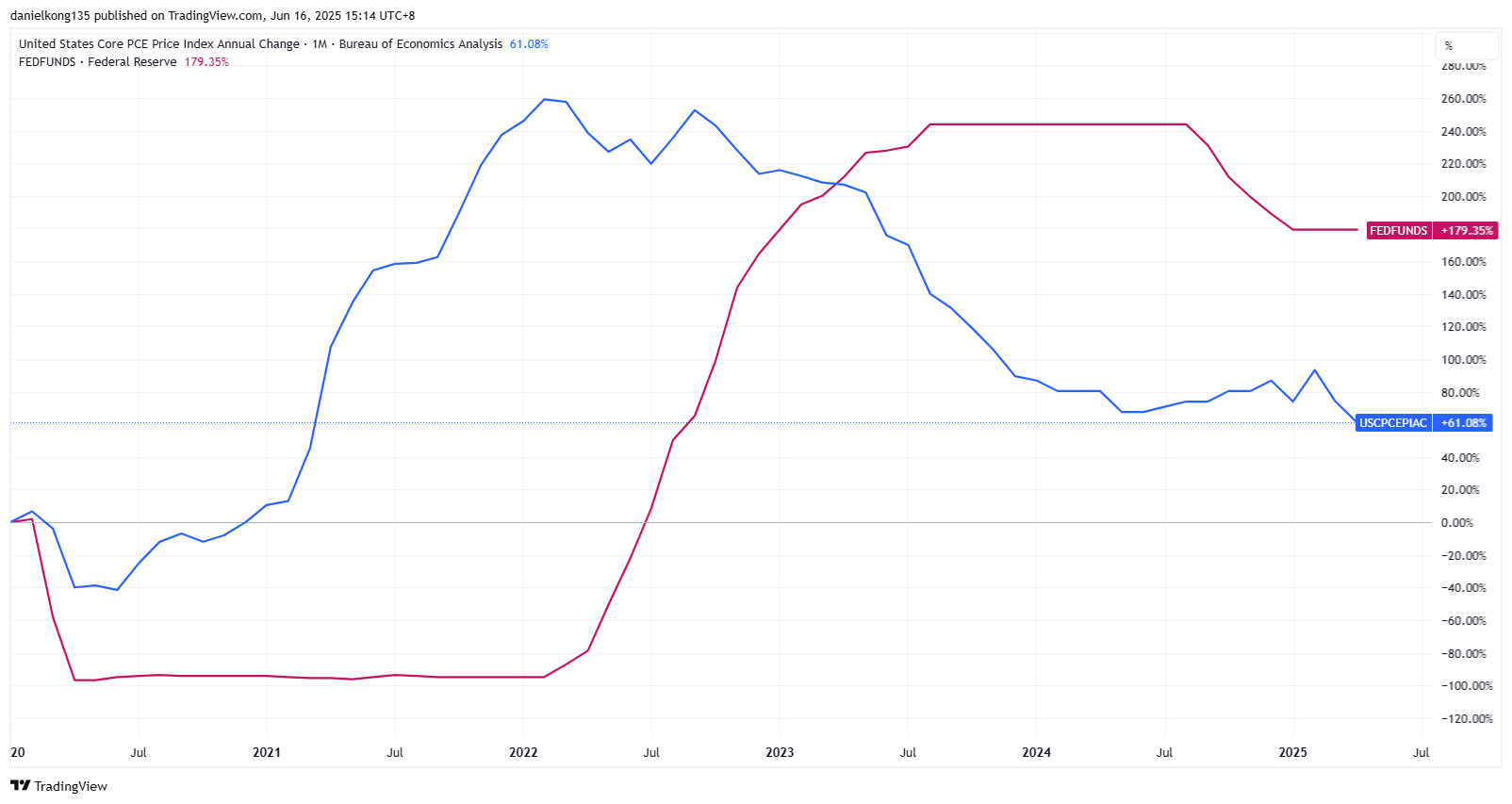

US Core PCE year-on-year vs Fed Funds Rate (2020 – 2025)

The chart above shows the Fed Funds rate (red line) rising steeply through 2022–2023, followed by a plateau in 2024–2025. Meanwhile, Core PCE (blue line)—the Fed’s preferred inflation gauge—has declined steadily from its peak but remains above the 2% target.

The lag effect is evident: while policy has tightened, inflation has only gradually responded, supporting the Fed’s cautious, data-dependent stance.

The historical playbook – When rates stayed high [5,6]

Today’s high-rate environment isn’t without precedent. Looking back, the most iconic “higher for longer” period came during the early 1980s under Fed Chair Paul Volcker. Interest rates were pushed above 15% in order to crush double-digit inflation, triggering a recession, but it worked.

Inflation eventually fell, and the economy reset. Fast forward to 2006–2007, the Fed held rates above 5% for over a year to cool a booming housing market. While inflation was more modest, the prolonged tightening contributed to financial imbalances that surfaced during the Global Financial Crisis (GFC).

In both eras, the impact of elevated rates rippled across employment, spending, and asset prices. Job markets cooled, corporate profits came under pressure, and equity markets struggled to sustain momentum.

In the 1980s, stocks remained choppy until the inflation threat truly receded. During the 2006–2007 period, markets initially held up but later unraveled as cracks in credit markets deepened. These episodes show that while the Fed’s stance may be necessary, the longer rates stay high, then the more fragile the economy becomes.

In some past instances, equity indices like the S&P 500 and Nasdaq 100 rebounded following inflation peaks and Fed signals, though this pattern is not guaranteed and outcomes may vary. In past cycles, markets have sometimes rebounded after rate peaks—though this is not guaranteed and may not repeat.

While short-term pain was common, There have been periods where markets rebounded after rate pressures eased, but this is not always the case, and past performance should not be relied upon.

Who feels the pressure? Sector-by-sector breakdown

With the Fed holding rates high well into 2025, markets are adjusting to a prolonged period of tight monetary policy. This “higher for longer” stance is reshaping the landscape across sectors— putting pressure on some, while others have shown more relative stability.

1. Technology & growth stocks

High-growth tech firms remain vulnerable to elevated rates. Valuations are under pressure as discount rates stay high, venture capital funding slows, and M&A activity stalls. While AI-driven names still attract interest, the pause in Fed easing extends the need for financial discipline.

2. Real estate

Real estate is directly impacted by high borrowing costs. Mortgage rates remain elevated, straining affordability and suppressing residential demand. Commercial property values are also adjusting, with REITs exposed to floating-rate debt and weaker tenants feeling the squeeze.

3. Banks & financials

Banks benefit from wider net interest margins but face growing risks. Deposit competition is eroding profits, while credit stress is emerging in commercial real estate and lower-income borrowers. Well-capitalised banks with diversified exposure are better positioned.

4. Consumer Credit

Consumers have held up well, but cracks are forming. Delinquencies on credit cards and auto loans are rising, especially among subprime borrowers. High rates are stretching household budgets, and lenders are beginning to tighten standards in anticipation of more stress ahead.

Is a September cut still likely? A look at the Fed’s dot plot and market forecasts

The Fed’s March 2025 dot plot projected two rate cuts by year-end, signaling a cautious but gradual path toward easing as inflation cools. While most FOMC members supported this view, a notable minority saw fewer or no cuts.

With the benchmark rate holding at 4.25%–4.50%, the updated dot plot, due at next week’s Fed meeting, will be closely watched as a key guide for how policy expectations are evolving.

Meanwhile, traders have resumed fully pricing in two cuts this year, buoyed by softer inflation data and rising jobless claims. Treasury yields have fallen sharply, with the 30-year yield down to 4.84%, reflecting renewed confidence in a potential September cut.

But with political pressure mounting, including fresh calls from President Trump for rate cuts, the Fed must now decide whether to reinforce its “higher for longer” stance or lean into the market’s more dovish view.

Global implications – Is the Fed exporting tightness?

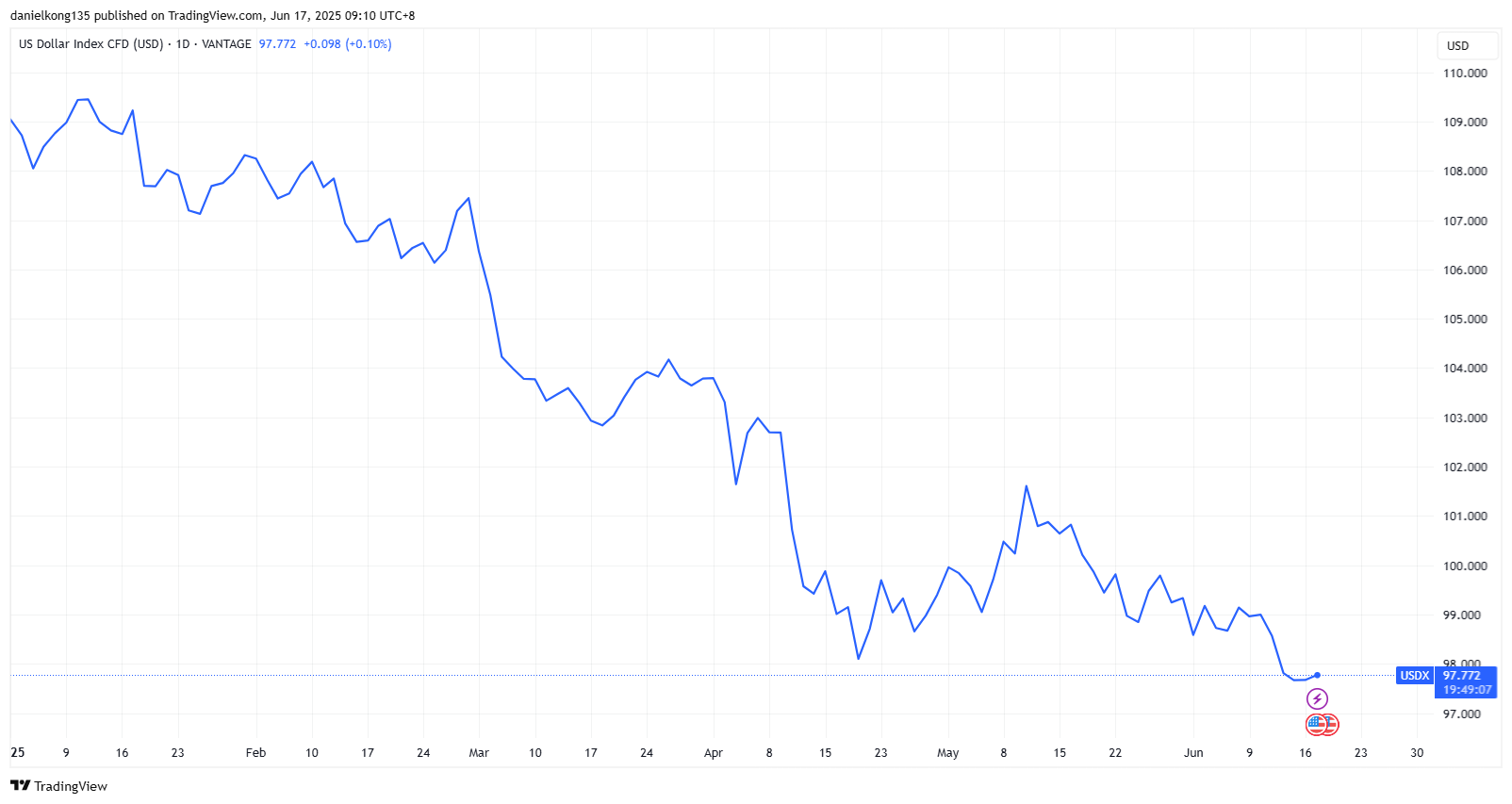

The US dollar has weakened nearly 10% in 2025, with the DXY index now around 97–98—its lowest level in over three years. The shift reflects a softening in Fed rate expectations, with markets pricing in two small cuts by year-end, even as the Fed maintains its “higher for longer” stance.

Adding to the pressure is renewed political noise, with President Trump ramping up calls for lower rates and a weaker dollar to boost US exports. While far from a full pivot, this shift has been enough to pull down the dollar, easing global financial conditions but stirring new risks elsewhere.

For emerging markets, a softer dollar offers some relief on dollar-denominated debt, but has also sparked capital outflows and currency swings.

Gold prices have climbed as investors hedge against dollar weakness, while oil prices have become more favorable in local currency terms, supporting demand across Asia and Latin America. Meanwhile, global central banks are diverging—the European Central Bank (ECB) has started easing, the Bank of Japan (BoJ) is holding steady but remains dovish, and the Bank of England (BoE) is cautiously cutting rates.

The result: rising FX volatility and a global market increasingly sensitive to even modest changes in the Fed’s tone.

Beyond the rates – Long-term lessons for investors

Monetary policy may move markets, but it’s not the whole story. In 2025, investors fixated on “when will the Fed cut?” risk missing the bigger picture. Corporate earnings remain resilient, innovation is pushing capex higher, fiscal spending continues to flow, and geopolitics are reshaping global dynamics.

History shows markets can rally even amid uncertainty—climbing that familiar “wall of worry.” With sentiment often diverging from data, some market participants highlight the importance of flexibility and awareness of long-term structural trends.

Reference

- “Fed holds rates steady as it notes rising uncertainty and stagflation risk – CNBC” https://www.cnbc.com/2025/05/07/fed-rate-decision-may-2025.html Accessed 16 June 2025

- “The US economy added a stronger-than-expected 177,000 jobs in April – CNN Business” https://edition.cnn.com/2025/05/02/economy/what-to-expect-from-fridays-jobs-report Accessed 16 June 2025

- “US Fed rules out pre-emptive rate cut while flagging tariff risks to inflation, jobs – The Straits Times” https://www.straitstimes.com/business/economy/us-fed-pauses-rate-cuts-again-and-flags-inflation-unemployment-risks Accessed 16 June 2025

- “Fed Well Positioned To Wait For Clarity On Outlook, Minutes Say – StreetInsider” https://www.streetinsider.com/Economic+Data/Fed+Well+Positioned+To+Wait+For+Clarity+On+Outlook%2C+Minutes+Say/24861388.html Accessed 16 June 2025

- “If interest rates are raised high enough to kill off inflation, how bad will the consequences be? – The Conversation” https://theconversation.com/if-interest-rates-are-raised-high-enough-to-kill-off-inflation-how-bad-will-the-consequences-be-189153 Accessed 16 June 2025

- “Federal Funds Rate History 1990 to 2025 – Forbes” https://www.forbes.com/advisor/investing/fed-funds-rate-history/ Accessed 16 June 2025